Canada's Housing Crisis: The Impact Of Steep Down Payments

Table of Contents

The Rising Cost of Down Payments and its Impact on Affordability

Down payment percentages, especially for higher-priced homes in desirable Canadian cities, have increased significantly in recent years. This surge has created a major hurdle for first-time homebuyers, who now face the daunting task of saving a substantial portion of a home's value before they can even qualify for a mortgage. The impact on affordability is undeniable.

The difficulty in saving for a large down payment is amplified by several factors:

- Increased competition among buyers driving up prices: The high demand for housing, coupled with limited supply in many areas, fuels a competitive market where buyers often need to offer above the asking price, further increasing the required down payment.

- Longer savings timelines needed to meet down payment requirements: Saving for a 20% down payment on a $750,000 home requires accumulating $150,000 – a significant sum that can take many years, even for dual-income households.

- Limited access to affordable housing options for low- and middle-income earners: The escalating cost of down payments effectively excludes many low- and middle-income individuals from the homeownership market, pushing them further into the rental market.

- Increased reliance on the Bank of Mom and Dad: Many Canadians now rely on financial assistance from their parents or family members to meet the down payment requirements, highlighting the intergenerational wealth gap.

Statistics paint a stark picture. For example, the average down payment in Toronto can exceed 25% of the home's value, while Vancouver presents an even more challenging landscape. This disparity across Canadian cities underscores the uneven impact of high down payment requirements on affordability.

Government Policies and their Role in the Down Payment Crisis

Government policies, while often intended to stabilize the housing market, can inadvertently contribute to the down payment crisis. For instance:

- Stress tests: Although designed to ensure borrowers can handle potential interest rate increases, stricter stress tests can make it harder for individuals to qualify for mortgages, even with substantial down payments.

- CMHC insurance premiums: While the Canada Mortgage and Housing Corporation (CMHC) insurance allows for smaller down payments (less than 20%), the premiums can add a significant cost to the overall mortgage, impacting affordability.

- Government grants and subsidies for first-time homebuyers: While these programs exist, they often fall short of addressing the core issue of high down payment requirements. Their limited availability and complex application processes further hinder their effectiveness.

Potential policy changes to address the crisis could include revisiting stress test criteria, adjusting CMHC insurance premiums, and expanding the availability and scope of government grants targeted at reducing the burden of down payments.

The Impact on Different Demographics

The high cost of down payments disproportionately affects specific demographics:

- Younger generations: Younger Canadians entering the workforce often face significant student loan debt and lower earning potential, making it incredibly challenging to save for a substantial down payment.

- New immigrants: Newcomers to Canada often require time to establish themselves financially and may face language barriers or a lack of credit history, further hindering their ability to secure a mortgage.

- Low-income families: Low-income families face the most significant barriers to homeownership, as the high down payment requirement represents a disproportionately large portion of their income.

Potential Solutions to Ease the Burden of Steep Down Payments

Several potential solutions can help make homeownership more accessible:

- Government initiatives to reduce down payment requirements: Governments could explore programs that allow for smaller down payments, potentially with increased oversight or risk-sharing mechanisms.

- Expansion of affordable housing programs: Investing in and expanding affordable housing initiatives can provide more options for individuals struggling to meet high down payment requirements.

- Exploring shared equity schemes and co-operative housing models: These models could help more people access homeownership by sharing ownership costs and responsibilities.

- Incentives for developers to build more affordable housing: Government incentives for developers could encourage the construction of more affordable housing units, alleviating the supply shortage.

Conclusion:

The steep cost of down payments is a major contributor to Canada's housing crisis, creating significant barriers to homeownership for many Canadians. Addressing this requires a comprehensive approach. This includes government policy changes that create more flexible mortgage options, innovative financing solutions like shared-equity models, and a concerted push to increase the supply of affordable housing. By tackling the issue of steep down payments head-on, we can work towards a more equitable housing market where the Canadian dream of homeownership is attainable for all. We urge policymakers and stakeholders to prioritize solutions that alleviate the burden of high down payments and contribute to a more equitable housing market in Canada. Finding effective solutions to Canada's housing crisis, particularly regarding the impact of steep down payments, is crucial for a healthy and prosperous future.

Featured Posts

-

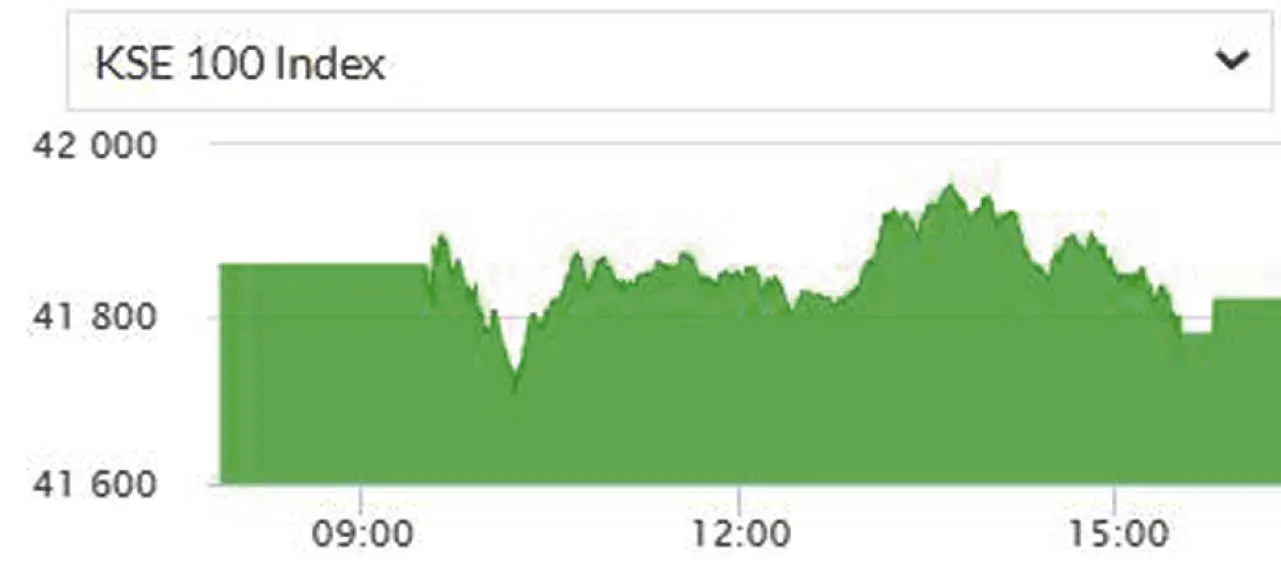

Pakistani Market Volatility Causes Stock Exchange Portal Outage

May 09, 2025

Pakistani Market Volatility Causes Stock Exchange Portal Outage

May 09, 2025 -

Golden Knights Defeat Blue Jackets 4 0 Hills Stellar Performance Leads The Way

May 09, 2025

Golden Knights Defeat Blue Jackets 4 0 Hills Stellar Performance Leads The Way

May 09, 2025 -

Nyt Strands Game April 9 2025 Clues Theme And Pangram Help

May 09, 2025

Nyt Strands Game April 9 2025 Clues Theme And Pangram Help

May 09, 2025 -

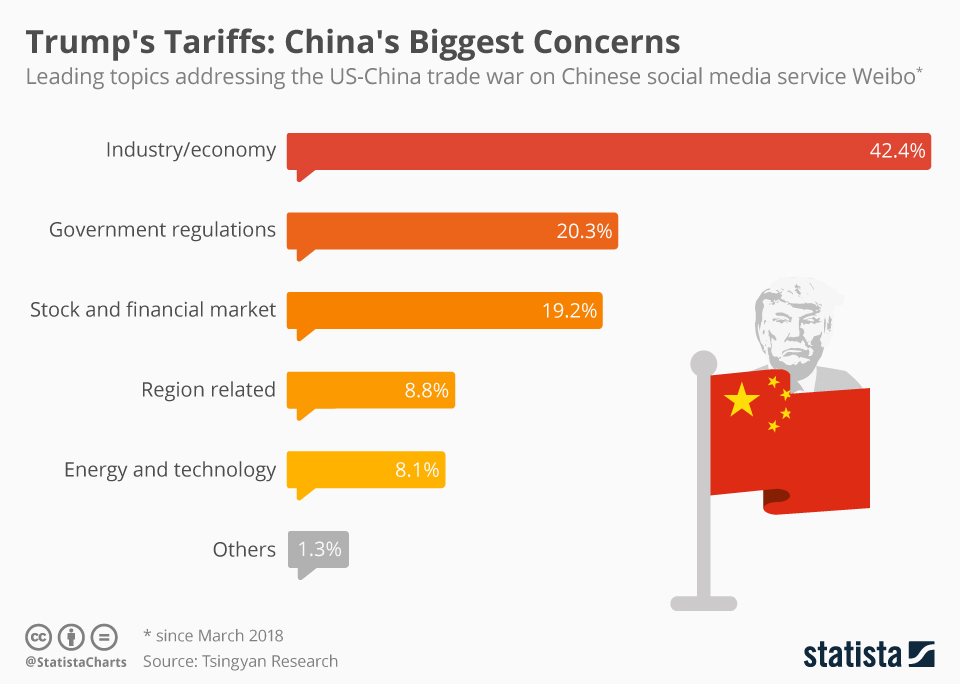

174 Billion Lost The Impact Of Trumps Tariffs On Global Billionaires

May 09, 2025

174 Billion Lost The Impact Of Trumps Tariffs On Global Billionaires

May 09, 2025 -

How Teslas Rise Increased Elon Musks Wealth After Dogecoin Announcement

May 09, 2025

How Teslas Rise Increased Elon Musks Wealth After Dogecoin Announcement

May 09, 2025