Escape To The Country: Financing Your Rural Dream

Table of Contents

Understanding Rural Property Financing Challenges

Financing a rural property presents unique challenges compared to urban properties. Lenders often perceive higher risk due to several factors, resulting in stricter requirements and potentially less favorable terms. Successfully navigating these hurdles requires careful planning and a thorough understanding of the landscape.

-

Appraisals may be lower due to limited comparable sales: Finding similar properties in rural areas for accurate appraisal comparisons can be difficult, potentially leading to a lower valuation than expected. This impacts the loan amount you can secure.

-

Lenders may require larger down payments: To mitigate perceived risk, lenders often demand higher down payments for rural properties, reducing the amount you need to borrow.

-

Rural properties sometimes lack access to crucial utilities: The absence of readily available utilities like high-speed internet, reliable water, or sewer systems can significantly impact a property's value and therefore its financing eligibility. This could necessitate additional upfront costs for infrastructure improvements.

-

Loan processing can take longer than in urban areas: Due to the complexities involved in assessing rural properties and the often lower transaction volumes, the loan processing time can be significantly extended compared to urban areas. Patience and proactive communication with your lender are vital.

Exploring Different Financing Options

Securing financing for your rural escape requires exploring various options. Each has its pros and cons, and the best choice depends on your individual financial situation and the specific property.

Traditional Mortgages

Conventional loans remain a popular choice for purchasing rural properties, but lenders often apply stricter criteria. Understanding the requirements and exploring options like USDA loans is crucial.

-

Requirements for credit score, debt-to-income ratio: Lenders typically require excellent credit scores (generally above 680) and a low debt-to-income ratio (DTI) to approve a conventional mortgage.

-

Down payment expectations: Expect a larger down payment (often 20% or more) for rural properties compared to urban properties.

-

Interest rate variations: Interest rates can vary depending on the loan term, credit score, and prevailing market conditions. Shop around for the best rates.

-

Loan term options: Traditional mortgages generally offer various loan terms, typically ranging from 15 to 30 years.

Rural Development Loans (USDA)

The USDA Rural Development loan program offers a valuable pathway to rural property ownership. Designed to support rural communities, it provides numerous benefits.

-

Low or no down payment options: USDA loans often require minimal or no down payment, making them significantly more accessible for many rural property buyers.

-

Lower interest rates than conventional loans: USDA loans frequently boast lower interest rates than conventional mortgages, leading to reduced monthly payments.

-

Eligibility requirements (income, location): Eligibility depends on your income level and the property's location within a designated rural area. Check the USDA's eligibility map to see if your desired property qualifies.

-

Application process and timelines: The application process can be more involved than a conventional loan, but the benefits often outweigh the effort.

Alternative Financing Options

Beyond traditional mortgages and USDA loans, alternative financing methods exist, each with its own set of advantages and disadvantages.

-

Seller financing: Negotiating directly with the seller to finance a portion or all of the purchase price can offer flexibility, but it's crucial to thoroughly review the terms and conditions.

-

Land contracts: These installment agreements allow you to make payments over time, giving you more time to secure additional financing or save for a down payment. However, it's vital to understand the risks associated with potential defaults or foreclosure.

-

Private money lenders: Private lenders might offer faster approvals and more flexible terms, but they typically charge higher interest rates.

Improving Your Financing Chances

Proactively strengthening your financial position significantly increases your chances of securing a loan for a rural property.

-

Credit score improvement strategies: Focus on paying down debt, maintaining timely payments, and monitoring your credit report regularly.

-

Saving for a substantial down payment: A larger down payment demonstrates financial responsibility and reduces the lender's risk.

-

Obtaining pre-approval from multiple lenders: Shopping around for the best terms and rates is essential. Pre-approval shows lenders your seriousness and strengthens your application.

-

Presenting a strong financial profile: Gather all necessary documentation, such as tax returns, pay stubs, and bank statements, to demonstrate your financial stability.

-

Understanding property value and potential issues: Thoroughly research the property's value and address any potential issues that might deter lenders, such as needed repairs or structural concerns.

Conclusion

Securing financing for your escape to the country requires careful planning and a comprehensive understanding of the available options. From traditional mortgages and USDA loans to alternative financing methods, numerous pathways exist to help you realize your rural dream. Remember to carefully weigh the pros and cons of each option, improve your financial standing, and consult with experienced professionals.

Ready to make your "Escape to the Country" dream a reality? Start researching financing options today. Explore the different loan programs and consult with a mortgage lender experienced in rural property financing to find the best solution for your unique needs and secure your escape to the country. Learn more about Escape to the Country Financing and find the perfect rural property for you!

Featured Posts

-

Jonathan Groffs Just In Time Opening Lea Michele And Friends Celebrate

May 24, 2025

Jonathan Groffs Just In Time Opening Lea Michele And Friends Celebrate

May 24, 2025 -

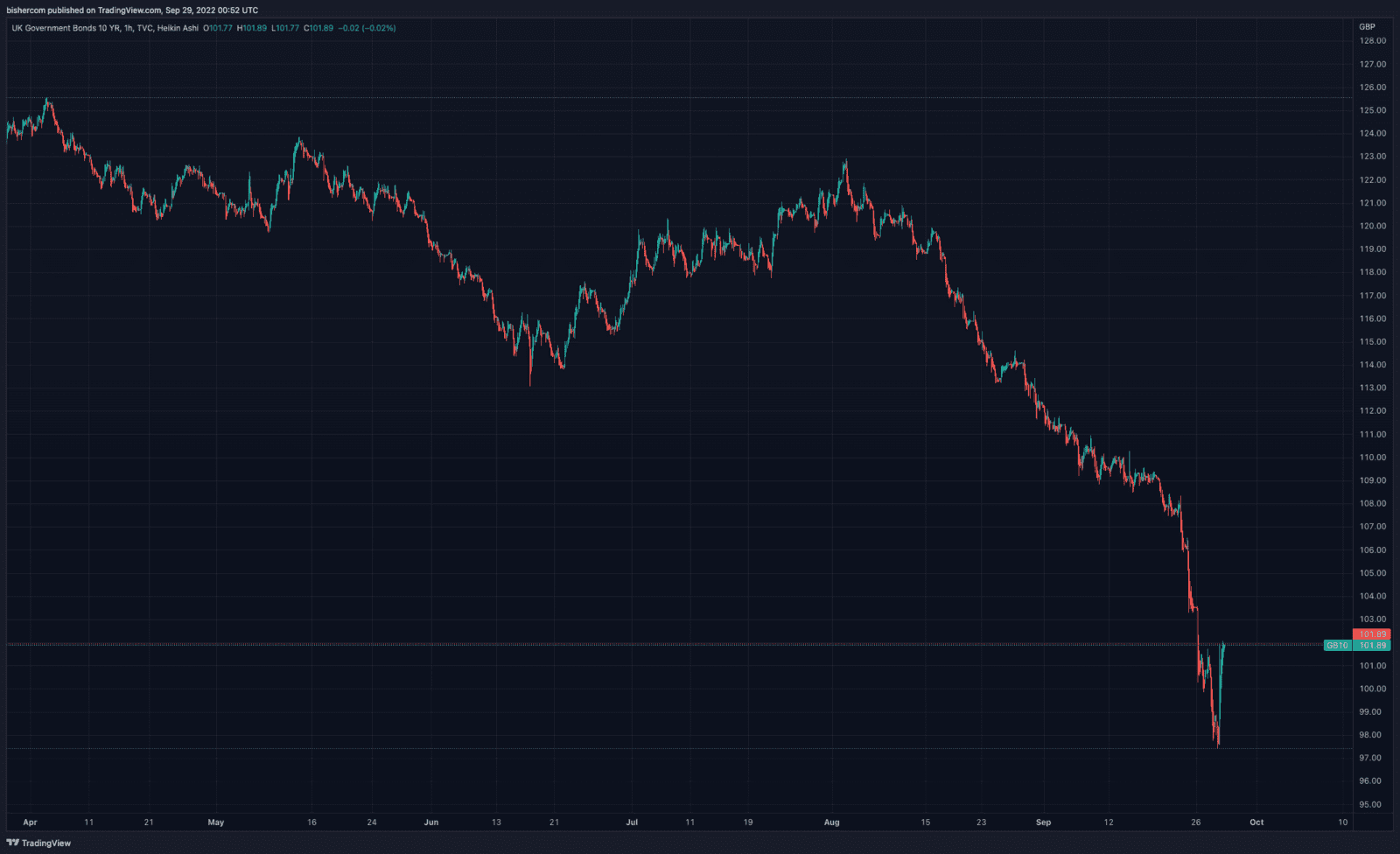

Is The Worlds Largest Bond Market On The Brink A Posthaste Perspective

May 24, 2025

Is The Worlds Largest Bond Market On The Brink A Posthaste Perspective

May 24, 2025 -

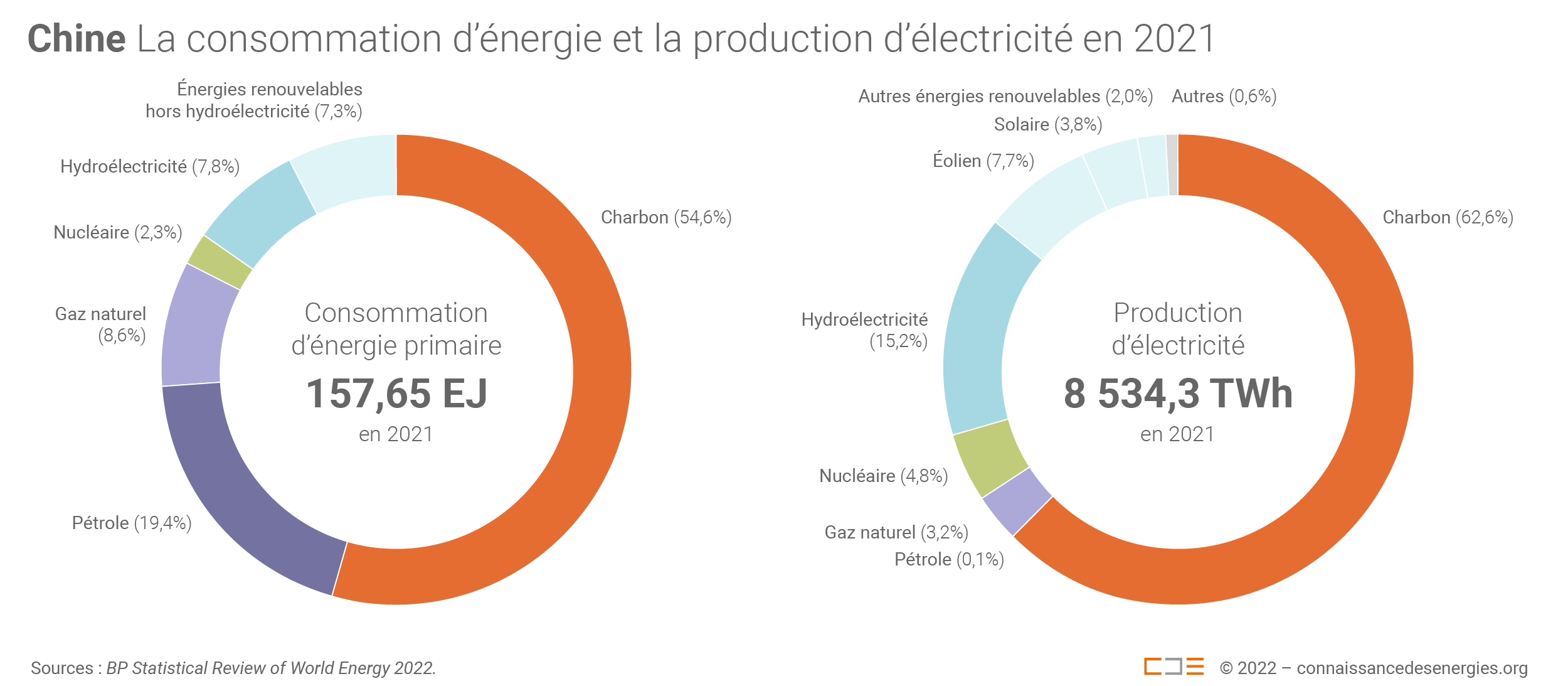

Silence Force La Mainmise De La Chine Sur Les Dissidents En France

May 24, 2025

Silence Force La Mainmise De La Chine Sur Les Dissidents En France

May 24, 2025 -

Top Rated Appliance Deals For Memorial Day 2025 Forbes Verified

May 24, 2025

Top Rated Appliance Deals For Memorial Day 2025 Forbes Verified

May 24, 2025 -

Joe Jonas And The Couples Hilarious Fight

May 24, 2025

Joe Jonas And The Couples Hilarious Fight

May 24, 2025